How Can We Help?

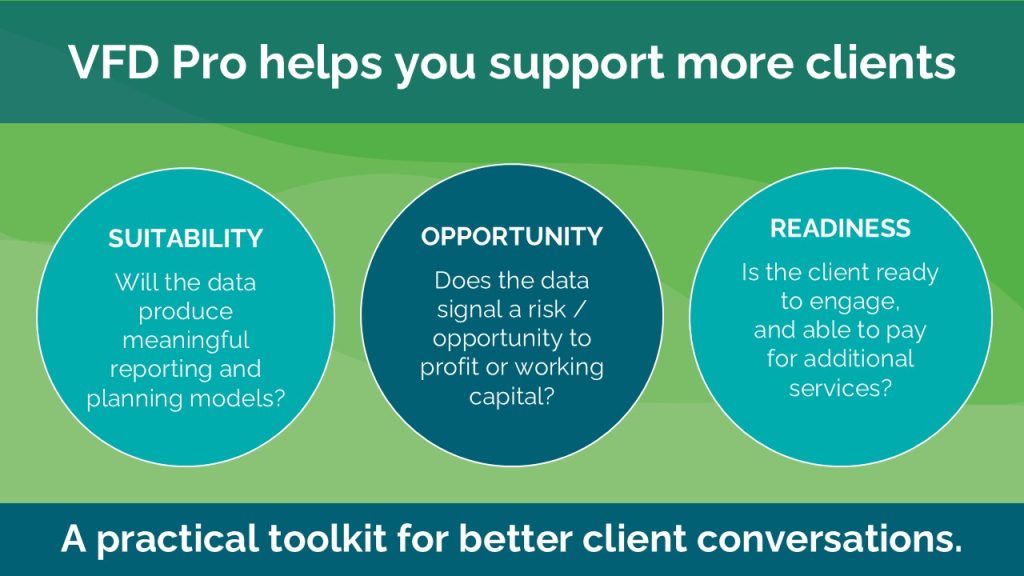

Client Discussion Model

Introduction

So What? Guide

The So What? Guide for the Client Discussion Model can be found here.

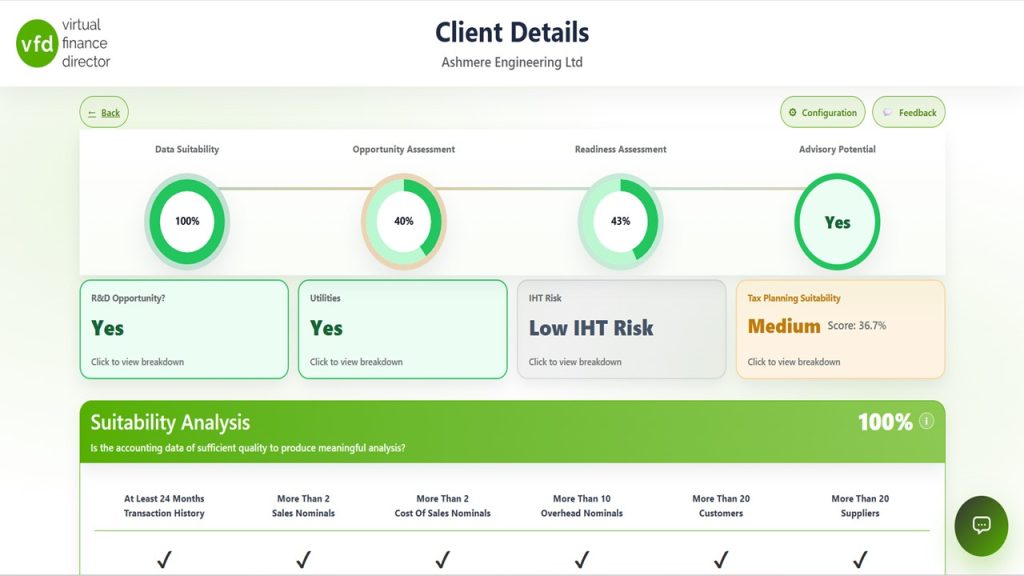

Example Model

To access the ‘Client Discussion Model’ please request a free trial of the VFD Pro platform – click here.

The model is available within the ‘Demo Reports’ area of your VFD Pro portal.

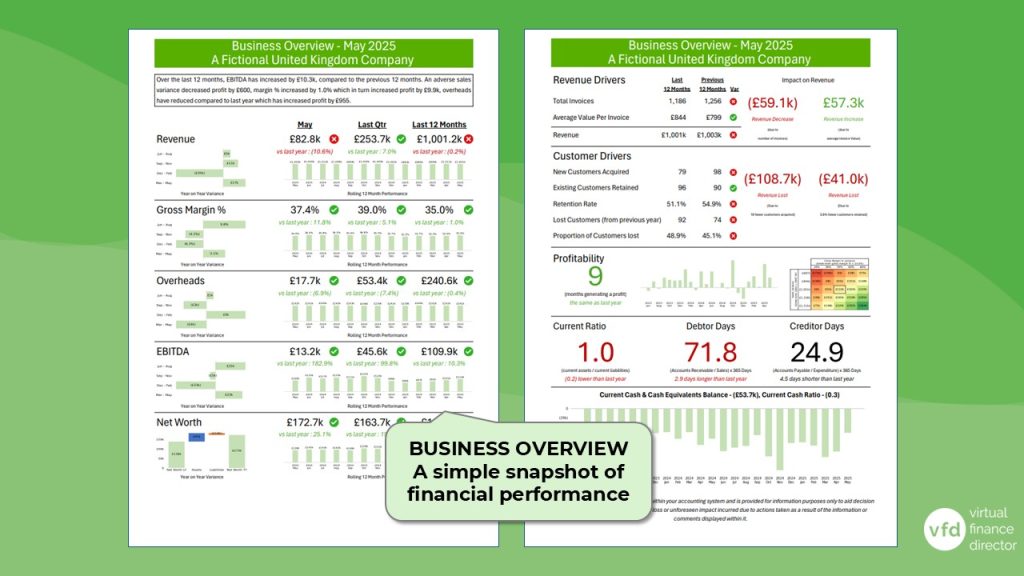

Report Overview

Below is a recording of the Client Discussion Model Webinar that was presented in April, demonstrating the potential of the Client Discussion Model.

The EVA Suite includes up to 7 different approaches to business valuation. These approaches are used to objectively determine the value of a small business based on its current financial performance trends. Here is a brief explanation of each approach:

Market Multiple Method: This method determines the value of a business by comparing it to similar businesses in the market. Key financial metrics such as revenue, earnings, or cash flow multiples are used to calculate the business value.

Comparable Transaction Method: Similar to the market multiple method, this approach looks at recent transactions of comparable businesses to determine the value. It considers factors such as the sale price, deal structure, and financial performance of these comparable transactions.

Discounted Cash Flow (DCF) Method: The DCF method calculates the present value of future cash flows generated by the business. It takes into account the estimated future cash flows and applies a discount rate to reflect the risk and time value of money.

Asset-Based Approach: This approach determines the value of a business based on its assets and liabilities. It considers the net book value of the company’s tangible and intangible assets, including property, inventory, equipment, and intellectual property.

Earnings Capitalisation Method: This method calculates the value of a business based on its future earnings potential. It considers the company’s historical earnings, projected earnings growth rate, and a capitalisation rate to estimate the business value.

Earnings Multiple Method: Similar to the market multiple method, this approach uses a multiple of the company’s earnings, such as the price-to-earnings ratio, to determine the value of the business.

Balance Sheet Valuation: This approach values the business based on its net asset value. It compares the company’s total assets to its total liabilities to arrive at the net worth or equity value of the business.

It’s important to note that the EVA suite allows for flexibility in selecting and combining these valuation methodologies based on the nature of the business, sector, and other relevant factors. The valuation range generated using these methods helps provide an impartial and fact-based estimate that can assist clients in understanding the worth of their business.